- July 7, 2026

- Posted by: admin

- Category: BitCoin, Blockchain, Cryptocurrency, Investments

Solana’s real-world asset transfer volume more than doubled over the past month, giving the network a stronger signal that tokenized assets are beginning to circulate rather than sit on-chain after issuance.

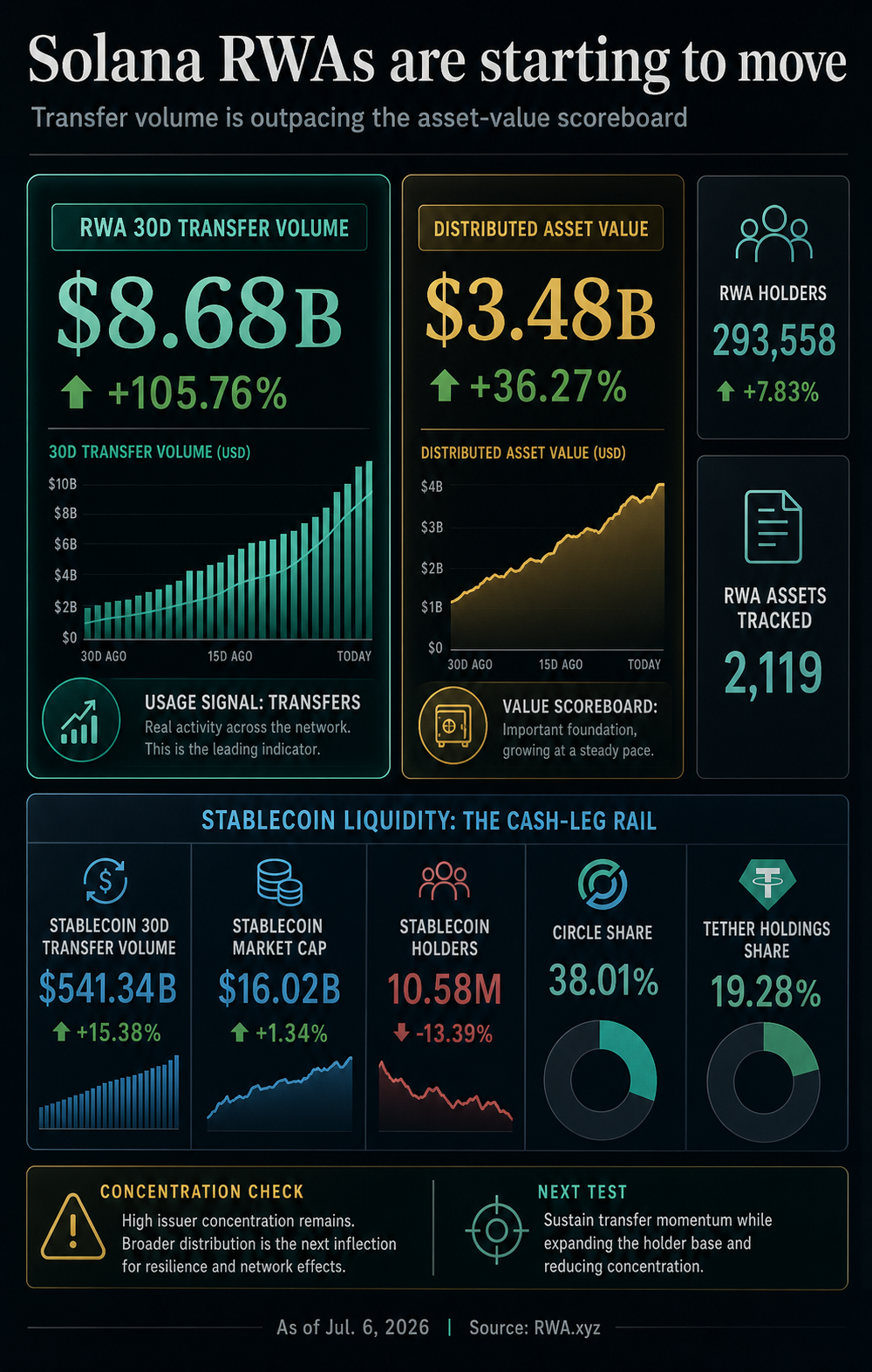

RWA.xyz showed Solana’s RWA 30-day transfer volume at $8.68 billion as of July 6, up 105.76% from 30 days earlier. Distributed asset value rose 36.27% over the same period to $3.48 billion.

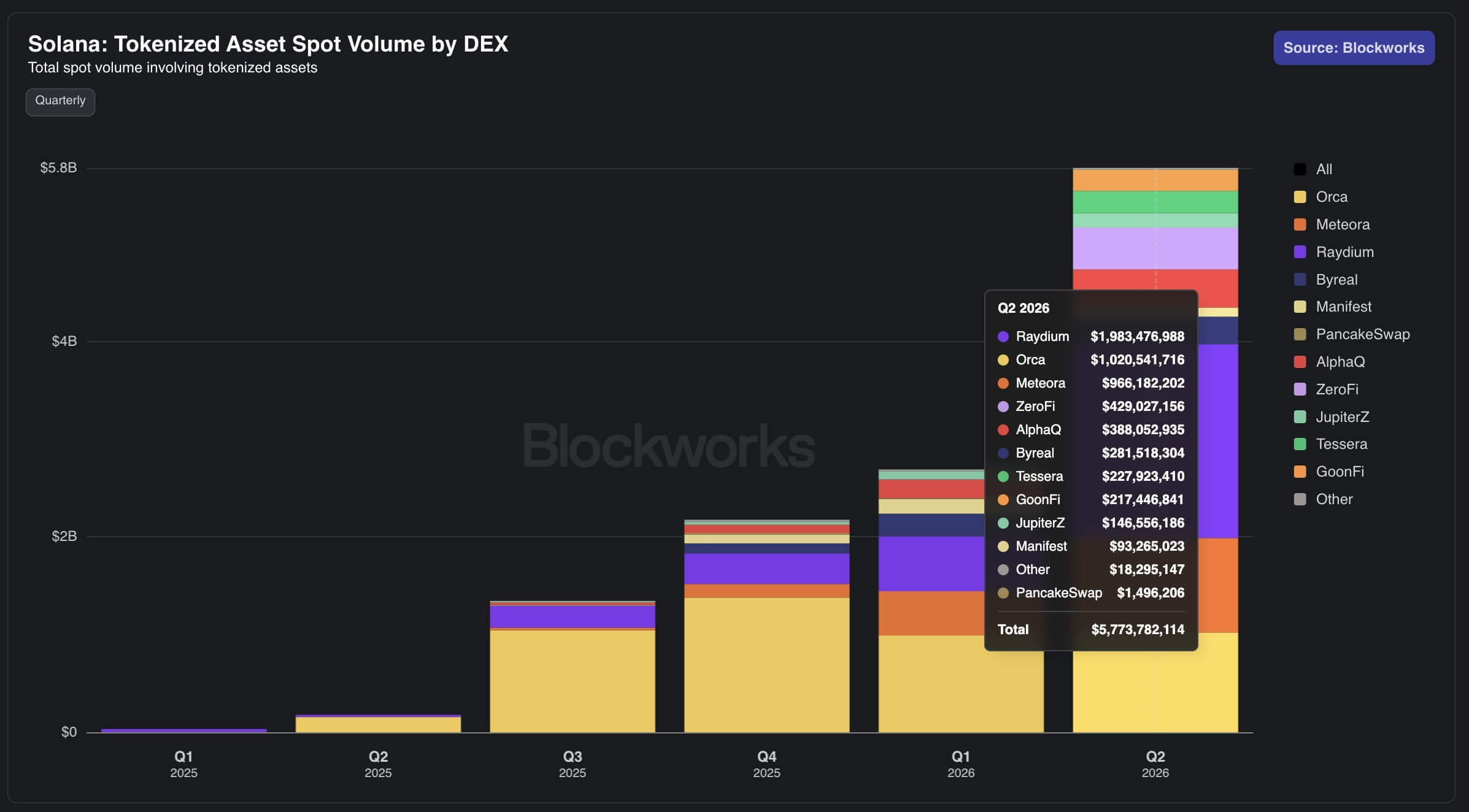

Solana’s own data showed a similar increase in turnover in a related market. The network said tokenized asset spot volume across decentralized exchanges grew from $2.69 billion in the first quarter to $5.7 billion in the second quarter. A year earlier, the figure was near zero.

Those figures are becoming more important as tokenization moves beyond early pilots. A tokenized fund share, equity wrapper or cash-equivalent instrument can increase a blockchain’s reported asset value when it is issued.

Moving those assets requires users, platforms or institutions to push them through trading, settlement, collateral or liquidity-management workflows.

Stock tokens bring a trading culture to Solana

Solana’s transfer surge has been helped by a broader holder base, giving the network more than an issuer-driven growth premise.

RWA.xyz showed Solana with 293,558 RWA holders, up 7.83% over 30 days, across 2,119 tracked assets. The increase was modest relative to the jump in transfer volume, but it showed that activity expanded alongside asset value rather than coming solely from changes in reported balances.

Part of that user growth followed the mid-2025 launch of tokenized xStock equities on Solana, which added a more retail-facing lane to a market often dominated by Treasury-style and institutional products.

xStocks, issued through Backed, brought tokenized exposure to individual US stocks and indexes onto Solana. The lineup includes shares tied to companies such as Tesla and Nvidia, two of the most closely watched names among retail traders.

Those products behave differently from tokenized Treasury funds or permissioned private credit instruments. Treasury-style products often appeal to institutions seeking yield, cash management or collateral.

Tokenized equities tied to volatile technology stocks can draw traders looking for familiar market exposure on crypto rails.

Solana’s low fees help make that activity more practical. Traders can buy, hold and transfer tokenized stock exposure without transaction costs overwhelming smaller positions, giving the network an advantage for retail-sized trades compared with chains where fees can rise sharply during periods of congestion.

The equity tokens did not create Solana’s RWA market, but they added an asset class with a stronger tendency to trade.

That gives the network a clearer explanation for why its latest RWA signal is showing up not only in asset value, but in transfer activity.

Institutional products anchor Solana’s RWA base

Solana’s RWA growth is also being supported by institutional products that add scale and credibility, even if they do not all generate the same level of transfer activity.

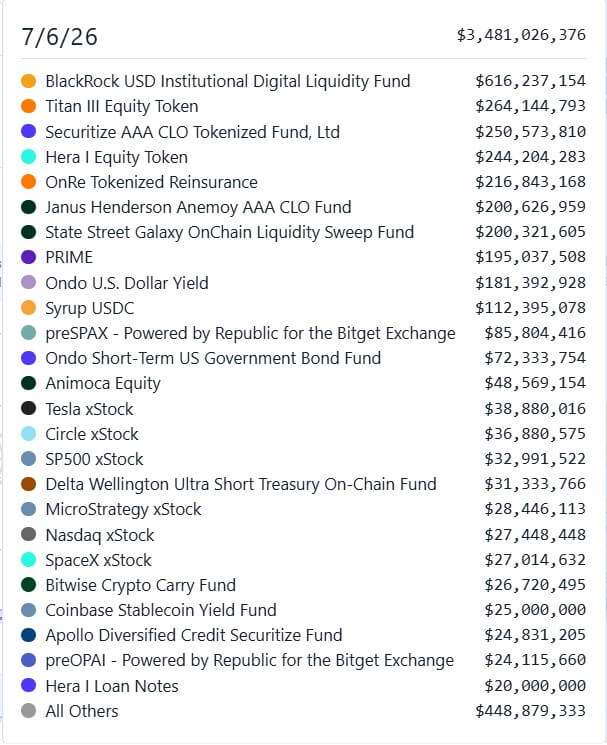

BlackRock’s BUIDL fund has $615 million in Solana assets, the largest RWA position tracked on the network. Ondo’s USDY has added another $181 million, giving Solana a deeper base of tokenized cash-equivalent and Treasury-style exposure.

Securitize-linked products have also become a meaningful part of the market, with nearly $300 million in assets under management on Solana.

The category includes exposure tied to regulated fund structures and credit products, adding another institutional layer to the network’s RWA footprint.

Those products bring recognizable financial names and more formal legal wrappers onto Solana.

Many operate through permissioned structures with know-your-customer requirements for minting and redemption, which can help attract institutional capital but may also limit how freely the assets circulate.

That distinction is important for the broader transfer-volume story. Large tokenized funds can lift Solana’s reported RWA value, but their contribution to market activity depends on whether holders use them for settlement, collateral, liquidity management or lending.

Private credit and specialty finance products can become more active when yield-bearing exposure moves into lending or collateral markets. Treasury-style products can support cash management and settlement, but their movement may remain more controlled because of compliance rules and investor eligibility.

The mix gives Solana a stronger institutional base, but it also keeps the transfer signal uneven.

The durability of the network’s RWA surge will depend on whether activity spreads across these products rather than remaining concentrated in a few large balances.

Solana’s edge is velocity, not scale

Solana’s recent RWA growth gives the network a clearer role in a market still led by Ethereum.

Ethereum remains the largest blockchain for tokenized real-world assets and has the deeper institutional footprint. Data from Token Terminal shows that the blockchain network controls 57.8% of all tokenized fund AUM, which currently sits at an all-time high of $35.6 billion.

This is because several traditional financial firms, including BlackRock and JPMorgan, built or tested their products on the network first, giving Ethereum an advantage in market history, integrations and institutional familiarity.

Solana is pressing a different claim. Its case rests on lower transaction costs, faster settlement and a market structure that can support more frequent movement.

Those traits become more important when tokenized assets are used for trading, collateral, liquidity management or settlement rather than simply held after issuance.

That distinction is central to Solana’s latest RWA signal. A large tokenized fund can raise a network’s reported asset value, but it does not automatically create market depth. Activity becomes more meaningful when assets move between wallets, trading venues, lending markets or collateral systems.

Solana’s stablecoin base supports that loop. RWA.xyz reported a stablecoin market capitalization on the network of $16.02 billion and a 30-day stablecoin transfer volume of $541.34 billion as of July 6.

That liquidity gives tokenized assets a cash leg for trading, settlement and collateral movement, though stablecoin holders fell over the same period, suggesting some activity may still be concentrated among larger wallets and platforms.

However, the network’s advantage remains incomplete. Legal and compliance limits still shape how far tokenized products can circulate.

Moreover, permissioned funds, private credit tokens and equity-linked instruments operate under different restrictions, with some limited by investor eligibility, redemption rules or off-chain legal structures.

That leaves Solana with a narrower but more defined opportunity. Ethereum still holds the deeper institutional base, while Solana is building its case around assets that benefit from cheap, frequent movement.

The next test is whether that movement spreads beyond a few large products and becomes a durable layer for settlement, trading and collateral.

The post Solana’s $8.7B RWA surge shows tokenized assets are finally starting to move appeared first on CryptoSlate.